Speak with an experienced advisor!

Speak with an experienced advisor! When should you truly consider whole life insurance. What is its best uses? When can one consider the cost of Whole Life Insurance to a good potential value? What are the Best Uses for Whole Life Insurance?

Great Questions. In my opinion, level term life insurance is such a great value for most Americans, it is hard to beat it. However there are some situations when a competitive and well structured whole life insurance policy from an A rated carrier can make sense. Of special note here, is that I am always both looking for and open to new ideas of when it can makes the most sense. Below, though, are the examples of situations when it can make great sense.

Things to Keep in Mind When Considering Whole Life Insurance:

In general when you are considering any whole life insurance policy, you should actively be comparing the cost vs the cost of the longest term policies that you can find, such as the thirty year.

The more expensive a life insurance policy is, the more time you should consider researching it.

Stay away from agents that get “pushy.”

Always research the insurer’s Financial Strength Rating.

Do not sign anything that you do not understand.

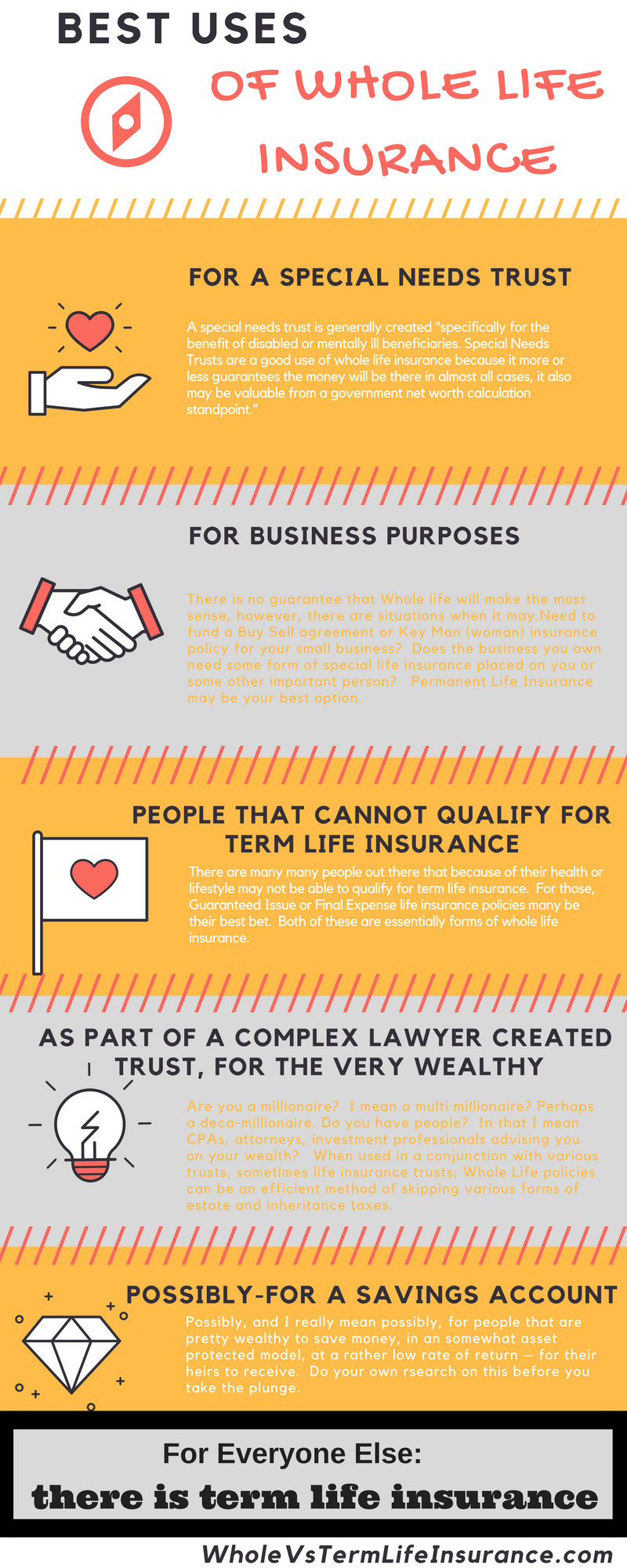

As part of a Business Requirement:

As part of a Business Requirement:

Need to fund a Buy Sell agreement or Key Man (woman) insurance policy for your small business? Does the business you own need some form of special life insurance placed on you or some other important person? Permanent Life Insurance may be your best option. There is no guarantee that Whole life will make the most sense, however, there are situations when it may. As with all life insurance, I would suggest that you get multiple quotes from different vendors before making a decision on this one. The health of the insured, the time frame, the age of the company, and the reason for purchasing it are all germane to the discussion. Compare and contrast both whole life policies and long term, perhaps 30 year term policies before deciding.

After receiving all of the quotes, again return to what the main goal for the life insurance policy was from the beginning. Try and not be led astray by new suggested requirements laid down by salesmen and other interested parties.

Special Needs Trust:

A special needs trust is generally created “specifically for the benefit of disabled or mentally ill beneficiaries.” This, according to Find Law: Special Needs Trust FAQs. If you find yourself needing to set up a Special Needs Trust, then yes, a Whole Life Insurance policy may be the best funding mechanism for it. In fact, in my humble opinion, I think this is clearly the best use of Whole Life Insurance. However all the details of who, when, where, etc need to be hashed out and as with most of my best possible uses of whole life insurance, you will certainly need a lawyer to assist you in its creation.

I believe that Special Needs Trusts are a good possible use of whole life insurance because it more or less guarantees the money will be there in almost all cases, it also may be valuable from a government net worth calculation standpoint. I cannot over emphasis however how special of a situation that this is. If you do not know what a special needs trust is, likley you do not need one. Again please Consult your CPA and lawyer.

People that can not qualify for level term life insurance policy:

There are many many people out there that because of their health or lifestyle may not be able to qualify for term life insurance. For those, Guaranteed Issue or Final Expense life insurance policies many be their best bet. Both of these are essentially forms of whole life insurance. Before you go down these directions, however, it may make sense to speak with a life insurance specialist about your health situation and your life insurance requirements first. There may still be avenues in purchasing a level term life policy. Please don’t give up to early.

So in theory, this form of whole life insurance may be the best option for those that do not qualify for term life. This form of life insurance though is not usually purchased for its cash value.

As part of a rather complex lawyer created Trust, often to pass along wealth from generation to generation.

Are you a millionaire? I mean a multi millionaire? Perhaps a deca-millionaire. Do you have people? In that I mean CPAs, attorneys, investment professionals advising you on your wealth? When used in a conjunction with various trusts, sometimes life insurance trusts; Whole Life policies can be an efficient method of skipping various forms of estate and inheritance taxes. There are other reasons for the super wealthy to create these trusts as well. Some of these other secondary and tertiary reasons are complex and intricate – speak with your licensed attorney.

Because whole life policies often are considered to be more “guaranteed’ than many other forms of monetary placement, they can be successful in reducing your risk from various unknown factors, and as a wealth transfer program. However, given that the current federal estate tax levels do not really begin until about $10.98 million for a couple, according to Forbes, then you probably will need a number higher than this before you consider this option. With all high end tax planning items though, its always best to consult your accountant and your lawyer. Various state and municipalities though also may have their own minimums.

Possible Use as a Savings Vehicle:

Possibly, and I really mean possibly, for people that are pretty wealthy to save money, in a somewhat asset protected model, at a rather low rate of return – for their heirs to receive. Not to be confused with the super wealthy trust creation model above. Of note is that this is in deed the classic example that many whole life insurance agents push. They often claim: Buy a whole life participating insurance policy, fully fund it and voila – you will have savings. The truth of course is it is not nearly that simple.

There are lots of notes and requirements tin my occasional acceptance of this as a ‘good use’. First off, this is only for people that each and every year fill up every tax free, tax deferred, health savings accounts (HSAs), college savings plans such as 529s, UTMA accounts, company differed income accounts, pay down their mortgage (if they have one), build up a hefty emergency account, AND have fully explored all the rest of universe of other savings options. I am not a financial planner, however it would seem to me that if you were looking to consider a whole life policy as an additional vehicle you would need to compare it to your other savings options. One of these of course should be tax advantage municipal bonds and bond funds. Another option would seem to be tax efficient broad market ETFs. There are of course other options such as rental properties. These three options include investments with tax advantages, which is sort of what whole life insurance for savings is considered. I personally do not really consider whole life insurance to be an investment, however it may be worth comparing it to these investments.

For a dual earning family that have access to 401ks, Roth Accounts, 529s, UTMAs, extra pay down of mortgages, etc – you are probably looking at clients that are saving over $70,000 to $80,000 per year- each year. Take to the extreme, it may mean only people saving over $120,000 per year. For single earning families this number will be smaller.

Of note with this opinion, is that the Whole Life policy really must be paid each and every year for it to have much savings value, otherwise the the cash account will end up up being used to pay for a non payment year and the numbers generally no longer make sense. Also since you must put money into a typical whole life policy for about 15 years before starting to see the fruits of your labor, this essentially means that you must be able to foresee paying all of your tax deferred and tax free accounts and then the hefty whole life premium, with no interruptions for about 15 years in a row, at least. From a long term financial planning perspective I find this nearly impossible to know with any certainty. Therefore I take issue with making this suggestion.

How to Buy Whole Life Insurance:

Whole, vs Term Life is extremely complicated to buy. With term life, it is rather hard to make an extremely bad insurance decision. Whole life on the other hand requires much more effort on the buyers part. First off, whatever you do, do not just buy the first whole policy from the first insurance agent that you speak with.

- Shop Whole Life Policies from numerous Insurance Companies.

- Shop Whole Life Policies from numerous Insurance Agents.

- Check the Financial Strength Rating from whomever you are considering purchasing from. Focus on A rated carriers.

- Do not believe the hype and ridiculous claims that many life insurance agents make.

- Let the numbers speak for themselves. Review again and again the guaranteed value charts. Compare Assumed value charts with similar assumed values.

- Do your homework and ask lots and lots of questions

- Fully consider term life before purchasing whole life.

- Do not sign anything that you do not understand.

- Get Quotes from lots of different agents and insurers.

Conclusion of Best Uses Whole Life Insurance

There you have it, a few real good reasons to consider purchasing Whole Life Insurance. I do really consider these to be the Best Uses Whole Life Insurance.

Consumers that are big advocates of whole life insurance will notice that there is one specific reason that some might be life insurance that I did not mention, Life Settlements. Life settlements are essentially selling your cash value life insurance policy to a third party. Life settlements may (or may not) be the best option once you have had a policy for decades but in and of itself it is not a reason to purchase one.

Read all the documents before you take the plunge and as always, compare multiple options. What do I think everyone else should purchase? Read our blog frequently and should easily be able to see.

Kindly please read our privacy policy.

![]()